The cost of US business insurance varies widely, with policies ranging from a few hundred to several thousand dollars annually. Factors like industry, company size, and coverage needs significantly impact the premium.

Navigating the world of business insurance in the United States can be complex, with a myriad of options tailored to protect companies from various risks. Business owners must assess their specific needs, considering factors such as the nature of their operations, the number of employees, and the types of risks their business is most susceptible to.

Adequate insurance safeguards a business’s financial health by providing a safety net against unforeseen events like lawsuits, property damage, and theft. It’s essential for entrepreneurs to research and compare different insurance providers and policies to ensure they’re getting the best coverage for their investment. Engaging an insurance broker or consultant can also provide valuable insights tailored to a company’s unique needs.

Credit: www.businessinsurance.com

Introduction To Us Business Insurance Costs

Understanding the costs of US business insurance is vital for any company. It protects assets and offers peace of mind. Let’s explore what factors determine these costs and why insurance is a must-have for businesses.

The Importance Of Insurance For Businesses

Business insurance shields companies from unexpected events. It covers losses from accidents, natural disasters, and lawsuits. This protection is crucial for financial stability and long-term success. Here’s why:

- Asset protection: Insurance helps safeguard your business’s physical and intellectual property.

- Risk management: It manages risks that could otherwise be financially devastating.

- Business continuity: With insurance, businesses can recover and continue operations after unforeseen events.

- Legal requirement: Certain types of insurance are legally required in many states.

- Customer trust: Insurance builds trust with customers, showing that the business is responsible and prepared.

Factors Influencing Insurance Costs

Different factors affect the cost of business insurance. They make each business’s insurance needs unique. Here are the key factors:

| Type of Business | Industry Risks | Location | Business Size | Policy Coverage |

|---|---|---|---|---|

| What your business does | Potential hazards in your field | Geographical risks and regulations | Number of employees and operations scale | Extent and limits of the insurance policy |

Other factors include:

- Claim history of the business

- Employee roles and their potential risk exposure

- Deductibles and policy exclusions

Knowing these factors helps in finding the right insurance. It ensures you’re not overpaying for unnecessary coverage.

Types Of Business Insurance Policies

Navigating through the world of business insurance can be tricky. Choosing the right coverage is crucial for protection. Here, we explore the essential types of policies every business owner should consider.

General Liability Insurance

General Liability Insurance is a must-have for any business. It covers legal fees and settlements if your business is sued. Here are key points:

- Covers bodily injuries

- Protects against property damage

- Handles advertising injuries

This insurance is your first line of defense against common business hazards.

Professional Liability Insurance

Also known as Errors and Omissions (E&O) insurance, this policy is vital for service-based businesses. It protects against:

- Negligence claims

- Mistakes in services provided

- Failure to deliver promised services

Professionals like consultants, accountants, and lawyers often need this insurance.

Property Insurance

Property Insurance safeguards your business’s physical assets. Whether you own or lease your space, this insurance covers:

| Assets Covered | Examples |

|---|---|

| Buildings | Offices, warehouses |

| Contents | Equipment, inventory |

This insurance helps you recover from theft, vandalism, or natural disasters.

Choosing the right business insurance shields your venture from unexpected financial losses. Each policy serves a unique role in your business’s safety net.

Average Cost Of Business Insurance

Understanding the average cost of business insurance is crucial for any business owner. Many factors determine this cost. These include industry risks, business size, and annual revenue. Let’s break down how these aspects influence what you might pay for peace of mind and protection.

Industry-specific Insurance Premiums

Different industries face unique risks. This affects insurance premiums. A construction company might pay more due to higher injury risks. A consultancy may pay less, as their risks are different. Here’s a quick look at how industry impacts insurance costs:

- Construction: Higher premiums due to physical risk

- Retail: Moderate costs with inventory risks

- Professional Services: Lower premiums, focused on liability

Size And Revenue Impact On Costs

The size of your business and the revenue it generates can greatly affect insurance costs. More employees often mean higher premiums. Higher revenue can also increase liability and the need for more coverage. See the table below for a simple breakdown:

| Business Size | Expected Insurance Cost Range |

|---|---|

| Small | $500 – $2,000/year |

| Medium | $3,000 – $5,000/year |

| Large | $10,000+/year |

Businesses must assess risks and find suitable coverage. Proper insurance helps protect against unforeseen events. It provides security for the company’s future.

Factors Affecting Insurance Premiums

Understanding the factors that influence your business insurance premiums is crucial. The cost of insurance can vary widely. The right knowledge can help you budget effectively.

Location And Risk Exposure

Where you do business matters. Insurance companies assess the risk level of your location. High-risk areas may face higher premiums. Consider these location-based factors:

- Crime rates

- Weather patterns

- Proximity to fire stations

Cities prone to natural disasters might see increased rates. A safe, accessible location could lower your costs.

Claims History And Business Experience

A clean claims record can save you money. Insurers view past claims as indicators of future risks. More claims can lead to higher premiums. Your business experience also plays a role:

- New businesses may pay more due to a lack of history.

- Established businesses with a clean record benefit from lower rates.

Experience in managing risks effectively can result in more favorable terms.

Policy Limits And Deductibles

Choosing the right coverage limits is key. Higher policy limits offer more protection but come at a cost. A balance is essential. Deductibles also affect premiums:

- A higher deductible typically means a lower premium.

- Lower deductibles can lead to higher upfront costs.

Select limits and deductibles that match your business’s capacity to absorb risk.

Calculating Your Business Insurance Costs

Understanding the cost of business insurance can be complex. It’s crucial to get the right coverage. This ensures protection without overpaying. Let’s dive into how to calculate insurance costs for your business effectively.

Assessing Your Business Risks

Identifying potential risks is the first step. This varies based on industry, size, and location. Use this checklist to start:

- Review past claims and incidents.

- Analyze operations for potential hazards.

- Consult with employees on perceived risks.

After assessing, you’ll have a clearer picture of the necessary coverage.

Comparing Quotes From Different Insurers

Don’t settle for the first quote. Comparing different insurers is vital for the best rate. Here’s how:

- Collect quotes from multiple providers.

- Ensure each quote is for comparable coverage.

- Look at customer reviews and financial stability.

By following these steps, you can find an affordable plan that doesn’t skimp on protection.

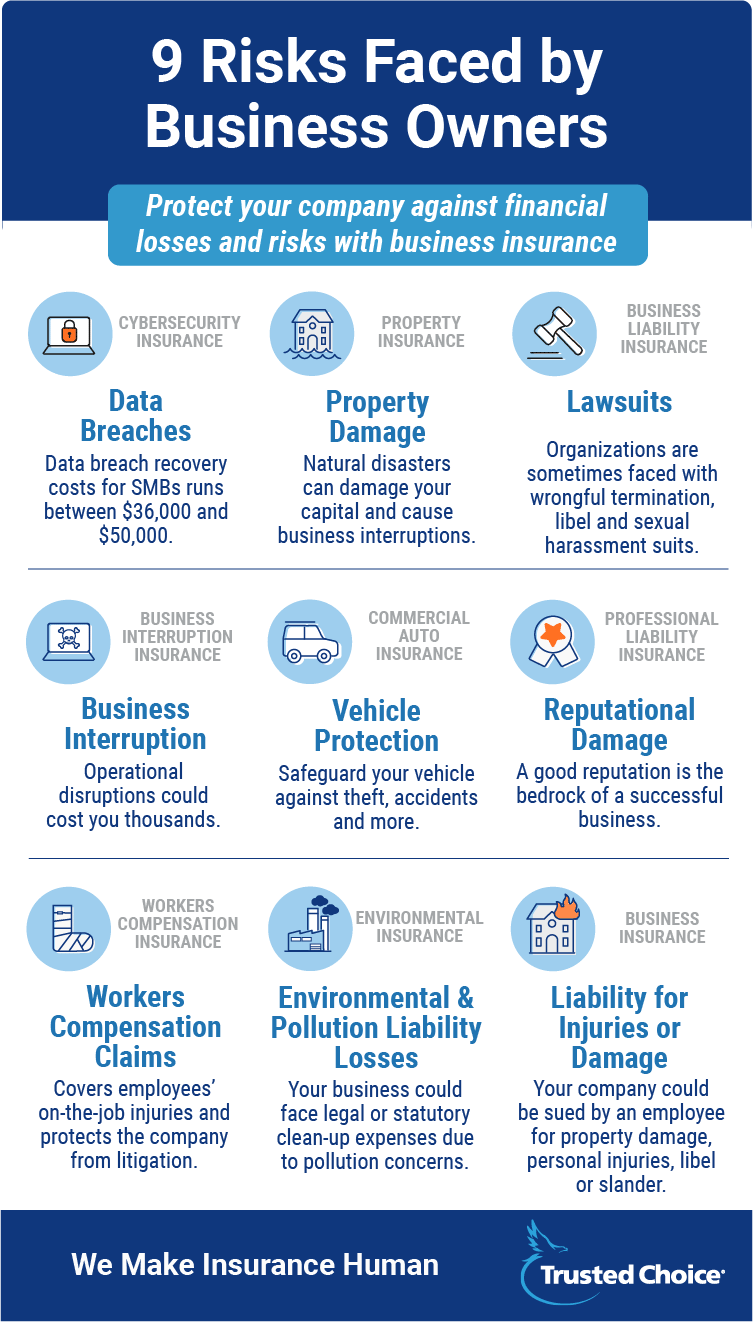

Credit: www.trustedchoice.com

Ways To Reduce Insurance Costs

Managing costs is key for any US business, especially when it comes to insurance. Smart business owners always look for ways to save without compromising on coverage. With the right strategies, reducing insurance costs can be straightforward and impactful.

Risk Management Strategies

Implementing risk management can lead to significant savings on insurance premiums. A well-designed plan reduces the likelihood of claims, which in turn can lower insurance costs. Consider these steps:

- Conduct regular safety audits to identify potential hazards.

- Train employees on best practices to prevent accidents.

- Invest in security systems to deter theft and vandalism.

Bundling Policies

Bundling multiple policies with the same insurer can unlock discounts. Insurance providers often offer reduced rates when businesses buy more than one type of coverage from them. Examples include:

| Single Policy | Bundled Policy | Potential Savings |

|---|---|---|

| General Liability | General Liability + Property | Up to 10% |

| Commercial Auto | Commercial Auto + Workers’ Comp | Up to 15% |

Regular Policy Reviews And Adjustments

Reviewing and adjusting policies annually ensures coverage remains aligned with current business needs. This avoids paying for unnecessary coverage. Key actions include:

- Assessing changes in business operations or assets.

- Discussing updates with your insurance agent to find potential savings.

- Adjusting deductibles where appropriate to lower premiums.

Insurance For Startups Vs Established Businesses

Choosing the right business insurance is a critical step for any company. Startups and established businesses have different needs. Startups often work with limited resources and must make strategic decisions about coverage. Established businesses, on the other hand, deal with a broader range of risks. They must adapt their insurance as they grow.

Initial Coverage Decisions For Startups

Startups need to focus on essential insurance policies. These protect against the most common risks. A General Liability Insurance is a must. It covers legal fees and damages if your business is sued. Professional Liability Insurance, also known as Errors and Omissions (E&O) insurance, is crucial for service-based startups. It helps if a client claims your work caused them harm.

- General Liability Insurance – Covers legal fees and damages.

- Professional Liability Insurance – Protects against claims of negligence.

- Product Liability Insurance – Important if you sell physical goods.

Property Insurance protects your physical assets. For tech startups, Cyber Liability Insurance is critical. It covers losses from cyber attacks.

Evolving Insurance Needs For Growing Businesses

Established businesses face complex risks. As they expand, they encounter new challenges. They often need to add or adjust policies.

- Workers’ Compensation – Mandatory as soon as you hire your first employee.

- Commercial Property Insurance – More coverage as your business assets grow.

- Directors and Officers Insurance – Protects decision-makers as your leadership team expands.

Business Interruption Insurance becomes more important. It helps if you cannot operate due to unexpected events. Commercial Auto Insurance is necessary if you use vehicles.

Remember, as businesses grow, insurance needs change. Regularly review your coverage. Talk to an insurance professional to ensure your business is always protected.

Credit: www.insurancebusinessmag.com

Navigating Insurance Claims And Disputes

When it’s time to make a claim, knowing the process can make things smoother. Disputes can arise, but with the right steps, they can be handled effectively. Let’s dive into the details.

Steps In The Claims Process

Understanding the claims process is crucial for a swift resolution. Here’s what to expect:

- Report the incident to your insurer as soon as possible.

- Fill out the claims forms with accurate details.

- An insurance adjuster will assess the damage or loss.

- Review the adjuster’s report carefully.

- After evaluation, the insurer will approve or deny the claim.

- If approved, you’ll receive a payment for the covered amount.

Handling Disputes With Insurers

Sometimes, you might not agree with the insurer’s decision. Here’s how to handle disputes:

- Start by reviewing your policy thoroughly.

- Gather evidence that supports your claim.

- Contact your insurer to discuss the dispute.

- If unresolved, consider a third-party mediator.

- As a last resort, legal action may be necessary.

Remember, clear communication and documentation are key in resolving disputes with insurers.

Future Trends In Business Insurance Costs

Understanding future trends in business insurance costs is crucial for companies. These trends affect budgeting and risk management strategies.

Technological Impacts On Insurance Pricing

Advances in technology are reshaping insurance pricing. Here are key factors:

- Data analytics enhance risk assessment accuracy.

- Automated tools speed up claims processing, reducing costs.

- AI and machine learning predict risks better, influencing premiums.

This integration of technology helps insurers set more accurate prices.

Predictions For Premium Changes

Changes in business insurance premiums are expected. Here’s what experts predict:

| Year | Predicted Premium Change |

|---|---|

| 2024 | 5% increase |

| 2025 | 4% increase |

| 2026 | 3% increase |

These predictions help businesses plan for future costs.

Frequently Asked Questions

How Much Is A $2 Million Dollar Insurance Policy For A Business?

The cost of a $2 million business insurance policy varies based on factors like industry, location, and risk level. Typically, premiums can range from a few thousand to tens of thousands of dollars annually. Contact an insurance provider for a precise quote.

How Much Does 1 Million Dollars Of Business Insurance Cost?

The cost of $1 million in business insurance varies widely based on industry, location, and risk factors, typically ranging from $300 to $1,000 annually.

How Much Is A 5 Million Dollar Business Insurance Policy?

The cost of a $5 million business insurance policy varies based on factors like industry, location, and risk level. Typically, premiums can range from a few thousand to tens of thousands of dollars annually. Contact an insurance broker for a precise quote tailored to your business.

Why Is Commercial Insurance So Expensive?

Commercial insurance is costly due to high risk coverage, potential for significant payouts, and tailored policies for businesses. Legal requirements and industry-specific risks also contribute to higher premiums.

Conclusion

Navigating the cost of business insurance can be complex, yet it’s crucial for protecting your enterprise. Remember, premiums vary widely based on industry, size, and risk factors. To secure the right coverage at a competitive rate, seek personalized quotes and consider the long-term value of robust protection.

Smart insurance planning is an investment in your business’s resilience and growth.